How DFIs create impact in venture capital

Venture capital (VC) funds are a vital tool for development finance institutions (DFIs) to scale the innovations of impactful, early-stage companies. This has received little attention in academic research, so the recent paper by Andonov, Li and Smeets (2025) (hereafter referred to as “ALS”) entitled Do Development Financial Institutions Create Impact through Venture Capital Investments? is welcome.

Some of the findings resonate strongly with BII’s experience. In other areas we see things differently. ALS studies how DFI-backed VC differs from commercial VC, but we seek to be additional to commercial investors, not to outperform them as venture capitalists. We deliver impact not by investing in funds whose portfolio companies grow faster or introduce more advanced technologies than commercial VCs, but by focusing on the margins where we can make a difference. That often entails introducing VC into new markets.

ALS’ central idea is that DFIs should address market failures. Investments in growing businesses can create both benefits for society (e.g. good jobs) and costs (e.g. pollution). These social returns are often misaligned with private returns – meaning investors may pass up on things we’d like to see happen and do things we wouldn’t. ALS group market failures under four common DFI objectives, which we tackle in turn, below.

ALS study the universe of domestic and international DFIs. They assess the effectiveness of 344 DFIs with investments in 2,770 VC funds and 33,106 underlying investments, in 57 countries. Over two-thirds of the deals covered are in North America and Europe, with fewer than 6 percent in Africa. Roughly 40 percent of BII’s VC commitments are in Africa.

Objective 1: Building a VC ecosystem

A thriving VC industry demands a strong “ecosystem” of willing investors, trusted fund managers (general partners, or GPs), and growth-oriented entrepreneurs coming together in an environment supported by conducive laws and regulations and service providers (lawyers, diligence specialists etc.). ALS hypothesise that ecosystem-building by DFIs means doing the things that “conventional” VC investors usually see as too risky – backing new, underrepresented GPs in high-tech sectors. However, they find that DFIs are less likely to back new funds than commercial investors, which is taken as evidence that DFIs are more risk averse.

BII’s partnership-first approach to VC has seen us anchor first-time GPs, many of whom have gone from strength to strength – Pi Ventures and Stellaris Venture Partners, for example. A successful ecosystem needs a critical mass of GPs that work effectively with early-stage companies to deliver commercial success and impact. This is our goal, not maximising the number of GPs by focusing on first timers. Established GPs typically make better investment decisions and offer support and experience that early-stage companies need. New GPs do matter, particularly in underdeveloped markets, but new funds created by established GPs can also play a pioneering role. The first-order question – whether it is a first or fifth fund – is always: what does the market need to create impact?

ALS also find that DFIs contribute to VC ecosystems by being more likely to invest in funds with female partners, a top priority for BII’s VC programme. However, an aspect of ecosystem development that we see as critical, but which is missing from the paper, is the contribution of technical assistance (TA). BII Plus – our TA facility – provides support to GPs, including practical and actionable support to manage ESG risks. Helping GPs to propagate good business practices in the companies they invest in amplifies our impact beyond what we could do directly.

Objective 2: Supporting entrepreneurship and SMEs

ALS hypothesise that reaching early-stage SMEs in “high-externality” industries is central to DFI impact.[1] They find that DFIs are less likely to invest in firms seeking early-stage financing (pre-seeds, seeds, or angel investments) than conventional VC – interpreted again as a sign of risk aversion. The authors find that 15 percent of DFI VC deals are in early-stage companies. That compares to 71 percent of BII’s VC commitments being pre-series A (from internal data). Wavemaker Impact is one of our earliest-stage VC partners, with a focus venture building (pre-seed) to set up fast-growing, high-impact climate start-ups.[2]

The paper also suggests DFI-backed firms might expect faster rates of growth – thanks to TA and other support – but it finds no evidence of this. Commercial investors are motivated by financial returns, and commercial VCs prioritise businesses that can scale very rapidly. We also care about growth – growing firms create more jobs and supply more goods and services to more people – and we also want our GPs to be commercially successful. But impact and growth are not synonymous. We would support GPs with slower-growth strategies, when that results in greater and more durable impact, and we do not see a comparison against growth rates in commercial VC portfolios as a good test of our effectiveness.

However, ALS do find evidence that DFIs are more likely to invest in industries with high positive externalities (in developing countries), which is much more like how we think about impact at BII, as an emphasis on social returns. But wouldn’t prioritising social returns show up in lower financial returns? ALS find no evidence that DFI-backed VCs perform worse than commercial VC. This result is hard to interpret. Some DFIs, such as BII, are willing to tolerate lower returns for the sake of impact, however the classic risk-return relationship means that investment markets price assets so that greater risk is compensated for by higher returns. It is difficult to assess the concessionality DFI VC investments without risk adjustment.

Objective 3: Fostering innovation

Innovative investments create new markets, raise productivity and create knowledge spillovers – all of which are critical for economic development. ALS test the impact of DFIs against this objective by looking at investments in “cutting-edge” industries, defined as AI, robotics and automation, semi-conductors, and nanotechnology. They find no significant difference between DFIs and conventional investors in their allocation to such industries.

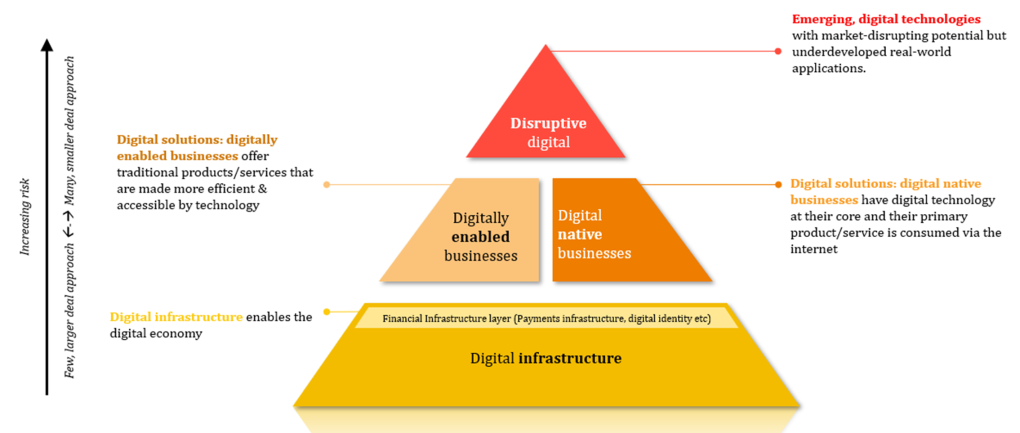

BII’s digital innovation strategy is built around the idea of the “digital stack” (see below). It captures “cutting-edge” technologies (disruptive digital), but also digital solutions for more efficient and accessible companies, and its foundation is core infrastructure, such as digital payments systems. ALS focus on the top of the stack, but BII takes a broader view.

ALS also find that firms receiving DFI financing are no more likely to become innovative over time, based on patenting activity. For BII, innovation in developing countries is often about new business models rather than patented inventions. For example, Basigo is an e-mobility start-up which we first invested in through the VC fund Novastar Ventures, and have since supported directly to expand into Rwanda. The technology is not “cutting edge”, but the innovation of making electric buses more affordable to operators through a “Pay-As-You-Drive” financing model – can deliver transformative impact without necessarily being at the global technological frontier. Other examples are fast-charging batteries to enable EV use in logistics and localised weather forecasting to enhance the resilience of smallholder farmers.

Objective 4: Promoting sustainable business

ALS hypothesise that DFI investments should result in more responsible business practices. They test this by comparing the number of corporate scandals (a proxy used for ethical business practices) and the number of firms that disclose emissions (the proxy used for environmental management) and find no difference with commercial VCs. The authors caution that these findings are “suggestive rather than conclusive.”

We do see encouraging responsible business practices as part of our role. We observe the impact of our work in this area through our engagement with fund managers and other actors. We have created a toolkit for VCs that includes due diligence and monitoring checklists, guidance on good governance and various ESG topics, and ESG management system templates. We also deliver practical training for first-time GPs to introduce ESG/risk management frameworks and for established managers to refine and improve. But it is not easy to observe the ultimate impacts of these efforts, as like ALS we see the need for further research in this area.

Conclusion

VC is a powerful but understudied weapon in the DFI arsenal. We therefore welcome research in the field and this recent paper from ALS captures some important areas of reflection for DFIs. BII has a long history of investing in impactful early-stage companies in challenging our markets, and we continue to evolve and learn from our portfolio.

[1] The authors define the following sectors as “high externality” according to the public economics literature: clean technology, health technology, education technology, agriculture technology, smart urban planning, infrastructure, shared economy, payment technology, and research & AI support.

[2] The need for public support is not necessarily greatest in earlier stages. Recent evidence from Aragoneses and Saxena (2025) illustrate the case for investing in later-stage VC where financial market imperfections result in insufficient scale-up financing. Through their structural model of European firms financed by publicly backed VC, they find that investing in “previously untapped markets with underdeveloped financial markets can yield large effects, but supporting later-stage VC there is necessary”