The Fourth International Conference on Financing for Development (FfD4) is taking place next year. The FfD3 agreement, struck in 2015, set the narrative that has guided development policy since. Next year we will need greater realism about the role of private finance.

Mobilising private investment is central to the role of development finance institutions (DFIs). It is also central to the achievement of global development objectives, such as the Sustainable Development Goals and Paris climate agreement. But the rhetoric around “billions to trillions” and mobilising private investment over the last decade has often been unrealistic and has created expectations against which development finance will inevitably be judged to have failed. FfD4 needs a positive but realistic vision of what concessional blended finance and private investment can achieve.

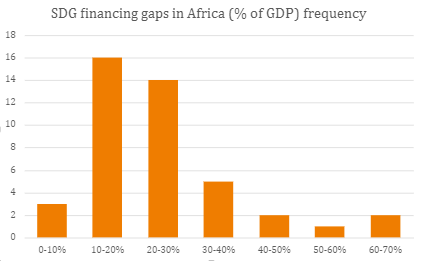

The Addis Ababa FfD3 agreement and the original articulation of “billions to trillions” by international financial institutions emphasised the importance of domestic revenue mobilisation and of public investment and spending, but that emphasis seems to have been lost since then. Private investment has sometimes been positioned as being capable of filling the gap between scarce public resources and estimated SDG financing needs, by “redirecting” a small share of trillions in global assets under management. That was never realistic. SDG financing gaps do not measure unmet demand for finance. The FfD4 conference must abandon the pretence that SDG financing gaps could ever be filled in this way, and instead focus on how the world can best make the most progress, starting from where it is now.

Filling SDG financing gaps would imply very large and sustained increases in national expenditures – a mix of private and public investment and public spending – in the order of 10 or 20 per cent of GDP in lower-middle income countries, and as much as 50 per cent of GDP or more in low-income countries. Spending increases of that magnitude would constitute a complete transformation of societies. Foreign DFIs and donors cannot deliver that simply by improving the supply of finance for private enterprises. Sustained investment booms require dramatic changes across government and society, it is not something outsiders can engineer.

Notes: Over half of African countries have annual SDG financing gaps above 20% of GDP. The lowest is Morocco (6%) the highest is CAR (65%). Source: authors calculations based on https://sdgfit.imf.org/

Private sector DFIs can only invest where there is a credible project that has a demand for finance, and meets important requirements on additionality, business integrity (anti-corruption) and environmental and social standards. The lack of “bankable projects” is now often noted. Project preparation facilities, technical assistance and blended finance can help get potential projects to the point where they are investable, but the underlying demand for investment has deeper determinants. For example, although in some countries there are incentives to replace incumbent fossil generation, investment in new renewable energy generation capacity will ultimately be driven by anticipated unmet demand for electricity. In the absence of demand investments will not happen. The relationship between investment and economic growth flows in both directions – investment is a proximate cause of growth, but growth also creates opportunities for investment. Making more progress towards filling SDG financing gaps will require making progress on the underlying drivers of economic growth.

At heart the purpose of concessional blended finance is to get more investment in places that need it, by enabling DFIs and private investors to invest where risks are relatively high and would otherwise be incompatible with their mandates and regulatory requirements. The measures of success should be the volume of investment, and whether the resulting development impact justifies the resources deployed and compares well to other potential uses of development funds.

Blended finance is most effective when applied to investments that are already reasonably close to meeting commercial investment criteria, so that only a relatively minor subsidy is required to create a viable investment. Proximity to commercial investment criteria also increases the probability that investors will take positive lessons from their experiences and will be willing to make similar investments without the need for further subsidies in the future. This sometimes involves the creation of new financial structures that can match investors with different risk-return requirements with investments in businesses at different stages of maturity, and that enable exposure to different risk-return positions within a given investment.

Over coming years, the largest volumes of private finance are most likely to be mobilised in the context of climate investments in middle income countries, because such investments are often already close to commercial viability. Within the set of countries in which DFIs have a mandate to invest, these are typically also the countries where carbon emissions are highest, and the need for investments to displace carbon intensive technologies is greatest. The fact that blended concessional finance and mobilised private finance are concentrated in middle-income countries is sometimes wrongly framed as a failing, but it reflects the reality of where mobilisation tools are both most effective and where investment is most needed to contribute towards climate goals.

There are opportunities to attract private finance into lower income countries, but those opportunities are fewer and typically involve smaller sums of capital. This reflects the fact that as a rule, many lower-income economies are smaller (have lower populations) and offer fewer and smaller investment opportunities. Those investments are also typically further away from commercial appetites which implies that trying to use blended finance to induce co-private investment would not be an efficient use of resources.

Blended finance is not only about the immediate mobilisation of private finance. It can also enable DFIs to make highly impactful investments that are further outside of commercial appetites, often in lower income countries or the riskiest market segments, than they would otherwise be able to undertake. Even though such investments may not result in reported private mobilisation, under existing reporting methodologies, these investments are about moving businesses and markets that are initially distant from meeting commercial investment criteria towards the point where they can attract private capital. They are about mobilisation over the long run. This is sometimes disparaged as DFIs “mobilising themselves” but that is mistaken. What ultimately matters is whether blended finance delivers on the overarching goal of increasing investments in places that need it, including investments made by DFIs alone.

Mobilisation targets and metrics are important, but they must also be used thoughtfully. Leverage ratios that are calculated at a transaction level using the face values of the public and private contributions can be misleading when they do not reflect the true cost to the public (the degree of concessionality). What appears to be a low leverage ratio can in some cases be highly effective mobilisation, when the public contribution represents only a small subsidy. What appears to be a high leverage ratio can be inefficient, when the subsidy conferred is large. Mobilisation ratios that are calculated at the portfolio level can be a poor indicator of how effective a DFI is at mobilising private finance, because DFIs’ portfolios include many investments where mobilisation, as reported under existing methodologies, is not the objective.

Quite what realistic expectations about the volume of private investment the DFIs can mobilise look like, is hard to say. BII and other DFIs must be ambitious and innovative, and continue to develop and work with efficient mobilisation vehicles, such as the ILX Fund, the $1.1bn SDG loan fund (developed by FMO, Allianz and Skandia) and the ADB’s Innovative Finance for Climate in Asia and the Pacific initiative, which is expected to unlock $10 billion in financing with the support of guarantees from European DFIs and governments. DFIs must set targets with the agreement of their shareholders, informed by the resources available to them and their view of market opportunities. The MDBs said at COP they plan to mobilise $65 billion in private climate investment annually in low and middle-income countries by 2030, for example. Bottom-up targets are a better basis for judging success than unrealistic “top down” goals.